As mobile traffic grows exponentially, operators continue to invest in 5G networks. By the end of 2022, the mobile market will have 1.23 billion smartphones and 6.9 million wireless devices, of which more than 600 million smartphones and nearly 1.5 million wireless devices are 5G.

Chinese mobile network operators maintain a rapid deployment of BTS in 2022, accounting for half of the global BTS deployment. Indian operators are aggressively deploying 5G networks. This will lead to radio unit deployments peaking in 2023 with more than 7.5 million units deployed globally. The RF component market for macro BTS will reach $3.2 billion in 2022 and is expected to grow to $3.8 billion by 2028. By 2023, we expect significant growth in volume and value, driven primarily by the rollout of 5G networks in India. The market volume is expected to continue growing on the back of higher penetration of massive MIMO antennas.

Sub-6 GHz small cells and 5G mmWave have many potential use cases, but these technologies have struggled to penetrate the market. Growth is slow because the industry is focusing on C-band massive MIMO deployments. Nonetheless, we expect small cells to grow steadily and substantially from 2024 onwards. The RFFE market for small cells and mmWave radios is expected to exceed $400 million by 2028.

NXP dominates the RF front-end market with a 35% share.

The top 5 RAN players (Huawei, Ericsson, Nokia, ZTE and Samsung) are consolidating their leadership positions. Huawei and ZTE increased their market share due to large-scale deployments in China, while Samsung leveraged its early-adopted v-RAN and O-RAN strategies.

The RF front-end ecosystem for 4G/5G wireless infrastructure is technically complex. Some players stand out with huge market shares, including: NXP, Qorvo, SEDI, and Analog Devices. NXP is the undisputed leader with a 35% market share in the overall RFFE market. At the wafer level, growth will be driven by IDMs such as NXP and Infineon, as well as major foundries such as GlobalFoundries, Tower Semiconductor and ST Microelectronics.

The U.S.-China trade war is polarizing supply chains in China versus the rest of the world. Therefore, China is accelerating the development of local supply chains, and more a

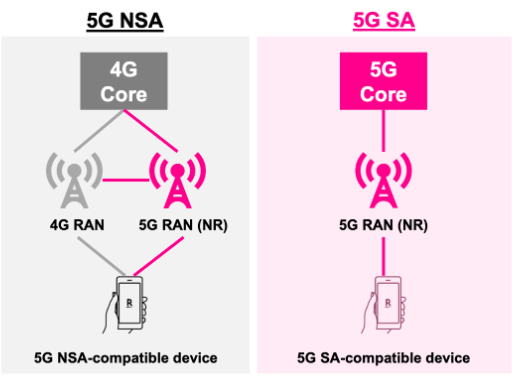

RAN is moving towards 5G STAND ALONE and massive MIMO

The start of 5G worldwide is Non-Standalone 5G (NSA) to ensure fast rollout and smooth coexistence with 4G LTE. 5G Standalone (SA) requires new investments, but enables new use cases such as network slicing, which MNOs can use for monetization.

Radios are using higher order MIMO systems, which greatly impacts the RFFE component count. The 10W and 5W PA modules of the 32T32R and 64T64R AAS have integrated drivers and pre-drivers, resulting in lower electronic power and higher levels of integration.

The need for power optimization is accelerating the transition to GaN-SiC final power amplifiers. Final stage PAs account for 45% of the RFFE market. GaN is more efficient than LDMOS, so most new AAS designs are based on GaN. With the support of Infineon’s PA modules, GaN-Si is expected to enter the mid-band massive MIMO antenna market.

Looking at the longer term, 6G research has already begun. From a technical point of view, the main challenge will be the transmission of terahertz frequencies (100 – 300 GHz), which requires new technologies, equipment and components. InP or SiGe are considered as potential technologies to realize 6G.

Post time: May-09-2023