Since the second half of last year, the chip industry has been taking a sharp turn for the worse, and everyone has no unified opinion on the recovery time of the industry. Recently, several giants have shown their pessimistic attitude without exception.

TSMC CEO Wei Zhejia told investors on Thursday’s quarterly earnings call: “The semiconductor inventory adjustment in the first half of 2023 is longer than we previously expected, and it may continue into the third quarter of this year before rebalancing to a more stable level.” healthy level”.

While issuing this warning, TSMC is facing the risk of annual revenue decline since 2009.

Peter Wennink, chief executive of Dutch advanced chipmaking equipment supplier ASML, said in a recent interview: “We are looking at . The “classic semiconductor down cycle” is being played out on a bigger stage. “

Although overall optimistic, their company’s orders in the first quarter also halved from the previous quarter. ASML’s backlog has been seen as rock-solid until mid-2024, but now appears to be weakening in the second half of 2024. The order book for the second half of 2024 isn’t full yet, but management expects (hopes) that it will.

“Never have more industries made semiconductors critical to their business,” Ben Bajarin, an analyst at consultancy Creative Strategies, said in an interview with the Financial Times. That means the chip industry is more volatile today than it was in 2008-2008. Much larger during the last recession in 2009.

“Some investors think this downcycle is built on top of a fairly long upcycle,” said Amit Harchandani, a semiconductor analyst at Citigroup. “Because the backlog has increased a lot, they’re concerned that the decline could be just as steep. There’s a bit of nervousness out there.”

Is this the “second down channel” of the semiconductor down cycle?

The way we’ve looked at the semiconductor industry for a long time is to look at things through two different components of supply on the one hand and demand on the other.

In our view, it’s clear that the “first round” of the current downcycle is largely supply-side driven, as the industry builds capacity like crazy after the Covid and supply chain crisis. The industry built and built, apparently recklessly giving up, until we “surpassed” the supply we needed, and now find ourselves in a state of oversupply, starting the current down cycle.

At the same time, the demand side has softened, perhaps with global macroeconomic concerns, and the downward pressure on demand has accelerated.

In our view, there is a good chance that the “second phase” of the current chip cycle will be driven more by weak demand than by oversupply in the first half of the year.

This can be worse because supply issues tend to be easier to solve than demand issues because if you’re a chipmaker you can control supply, as we’ve seen in the memory market with Micron and Samsung pulling capacity and products off the line to support pricing.

The problem is that the industry can do little to stimulate demand for chips. Lowering the price of automotive chips does not stimulate demand.

Electronics continue to decline, semiconductor future uncertain

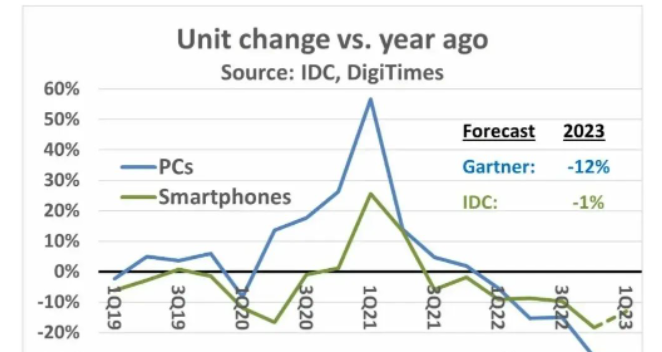

Shipments of PCs and smartphones will be weak in 2022 and continue to decline in 2023. IDC estimates that PC shipments will decline 29% year-over-year in the first quarter of 2023, following a 28% year-over-year decline in the fourth quarter of 2022. In 2022, PC shipments are down 16% from 2021, the largest year-over-year decline in PC history. The outlook for the remainder of 2023 is less favorable, with Gartner forecasting a 12% decline in PC shipments in 2023. The PC market crashed after a boom ended during the COVID-19 pandemic. Uncertainty in the global economy has contributed to the current weakness in the PC market.

IDC estimates an 18% year-over-year decline in smartphone shipments in the fourth quarter of 2022, leading to an 11% decline in shipments in 2022, the largest decline ever. Smartphones rebounded from a 7% decline in 2020 (driven by a pandemic-related production slowdown) to 6% growth in 2021. As with PCs, current economic uncertainty is impacting smartphone shipments. DigiTimes estimates that smartphone shipments will decline by 13% year-over-year in the first quarter of 2023. IDC expects smartphone shipments to decline by 1% in 2023.

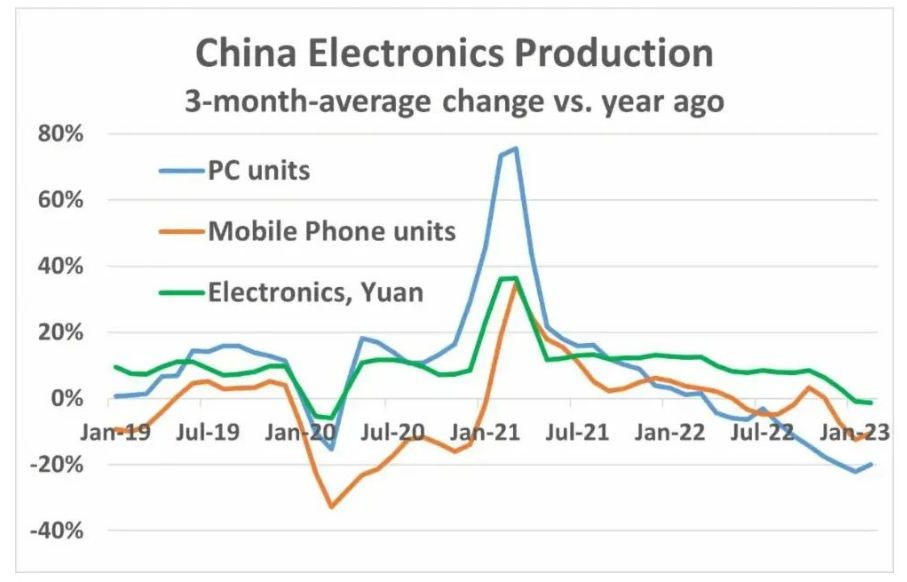

Weakness in PCs and smartphones was reflected in production figures in China. While some electronics manufacturing has shifted out of China over the past few years, China still accounts for about two-thirds of smartphone production (according to Counterpoint Research) and the vast majority of PC production. The three-month average change in PCs in China turned negative by April 2022 compared to a year ago (3/12) and declined more than 20% over the past three months to February 2023. Changes in mobile phone production (mainly smartphones) have been negative for seven of the past nine months, with declines of more than 10% in the last two months. In January 2023, China’s total electronics production measured in local currency (yuan) changed by 3/12, turning negative, the first decline since the early months of the pandemic in 2020.

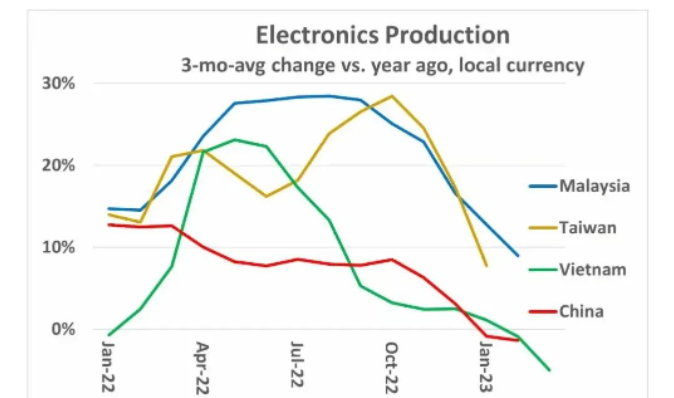

Countries benefiting from the relocation of electronics production out of China also saw a slowdown. Both Malaysia and Taiwan reported strong growth in electronics production for most of 2022, with changes mostly above 20% in 3/12 and approaching 30% in several months. In the latest data, the 3/12 rate of change fell below 10% in January for Taiwan and February for Malaysia. Vietnam’s 3/12 change in Q2 2022 was more than 20%, but decelerating every month since June 2022. Vietnam’s 3/12 change becomes negative 1% in February 2023, same as China. Vietnam is negative 5% in March 2023.

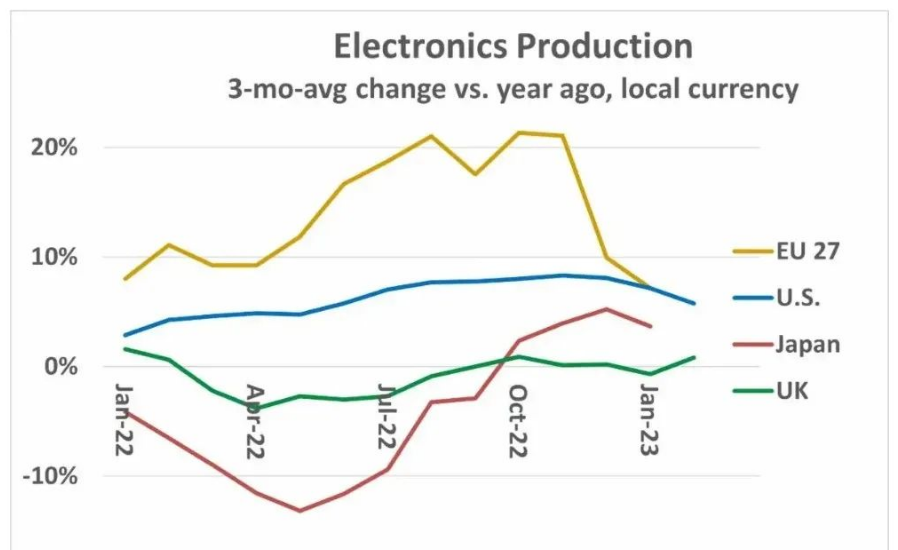

More mature electronics manufacturing regions were not affected by the slowdown in PCs and smartphones. The United States, Japan, the United Kingdom, and the European Union 27 countries (EU 27) are less dependent on consumer electronics. Electronics in these countries are primarily industrial, automotive, communications infrastructure, and enterprise computing. However, growth in many of these countries is slowing. Changes in electronics production in EU 27 3/12 are mainly between 10% and 20% for most of 2022. In January 2023, the 3/12 change drops to 7%. 3/12 U.S. growth accelerated moderately through most of 2022, from 3% in January 2022 to more than 8% in the last three months of 2022. U.S. growth has been decelerating through 2023, falling below 6% in February. In contrast, electronics production in Japan and the UK will decline for most of 2022. Japan 3/12 turns positive in October 2022, 4% in February 2023. UK 3/12 turns positive 0.9% in October 2022. After falling 0.7% in January 2023, the UK 3/12 rebounds to 0.8% in February 2023.

As stated in our February 2023 Semiconductor Intelligence newsletter, the outlook for semiconductors in 2023 is bleak. In addition to weak end demand in many electronics markets, many semiconductor companies are also facing excess inventory and pricing pressure. Despite some bright spots such as automotive (communication in March 2023), the overall semiconductor market will not recover until end demand for key end devices such as PCs and smartphones reverses its downward trend.

Post time: Apr-28-2023